Question 4

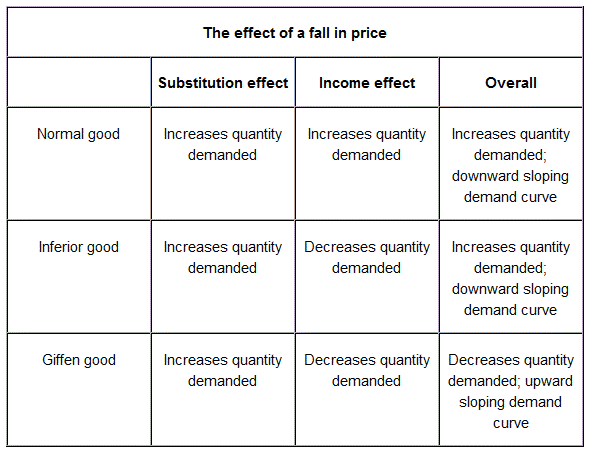

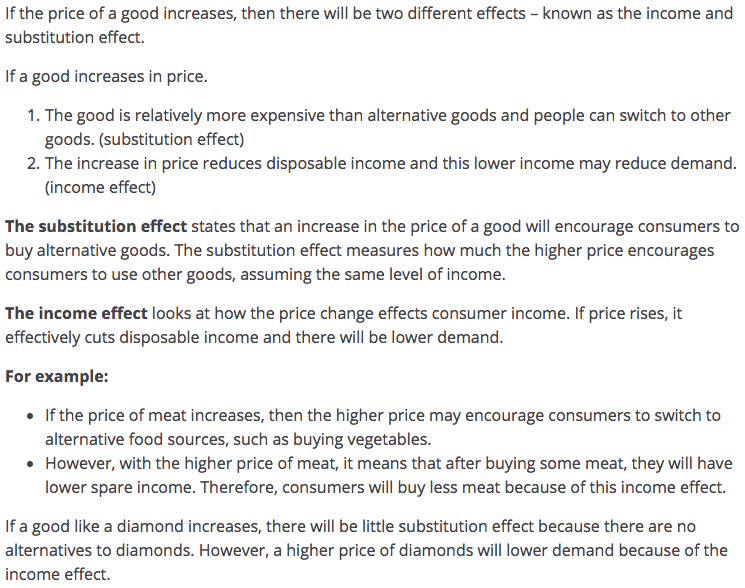

Substitution Effect and Income Effect

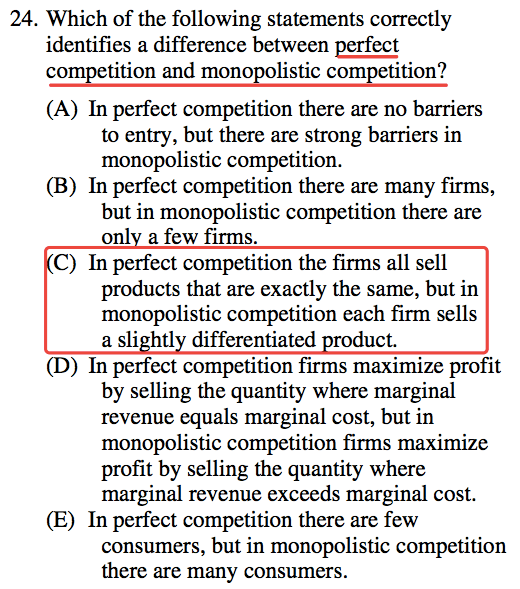

Question 24

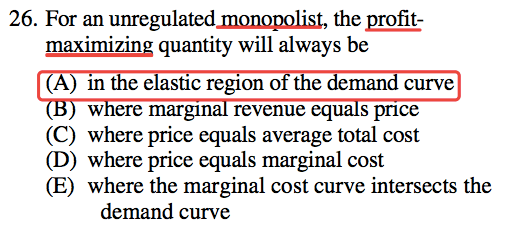

Question 26

Question 28

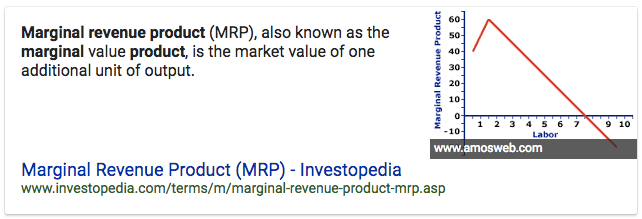

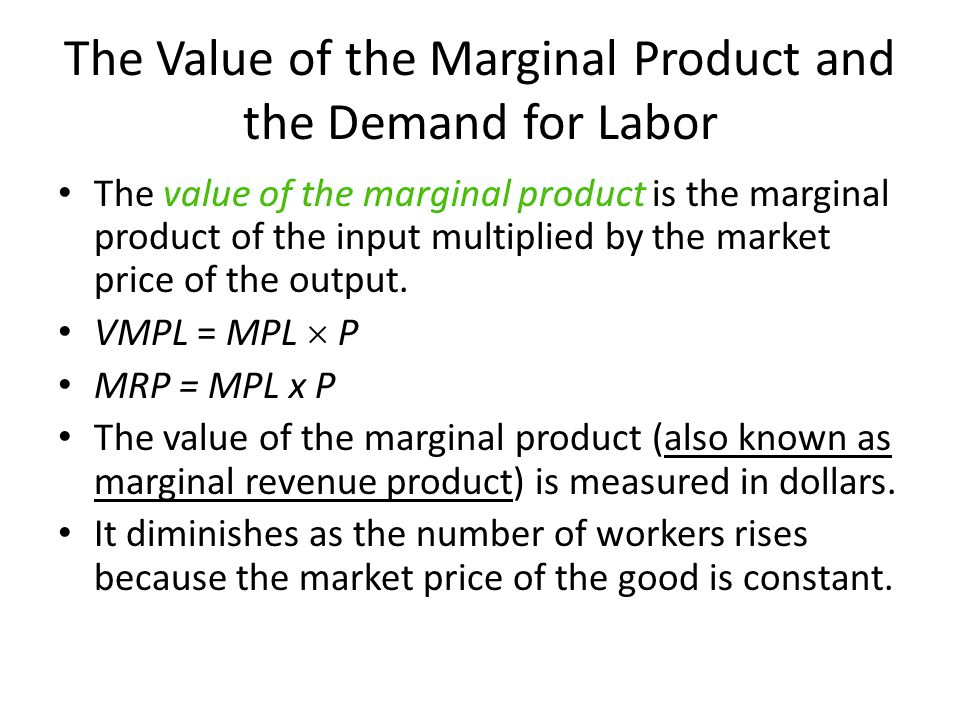

Marginal revenue product

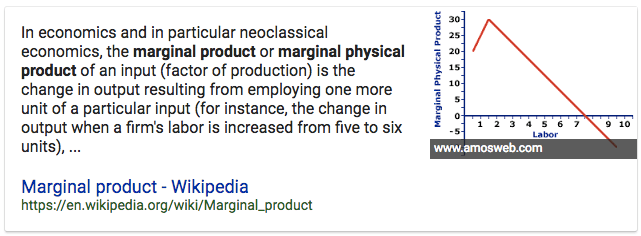

Marginal product

Relationship between Marginal revenue product and Marginal product

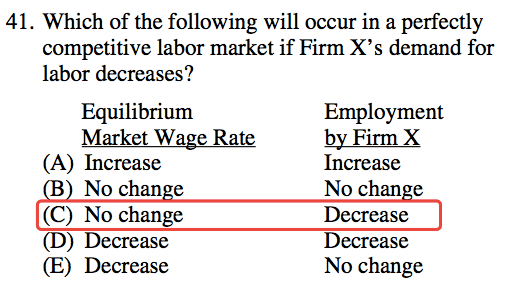

Question 41

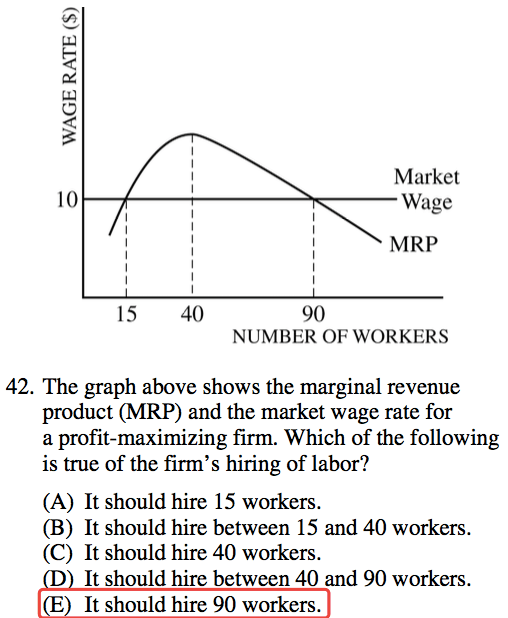

Question 42

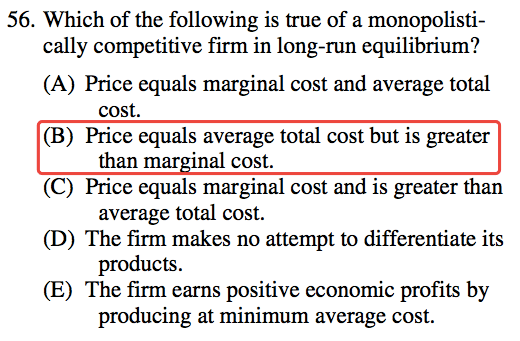

Question 56

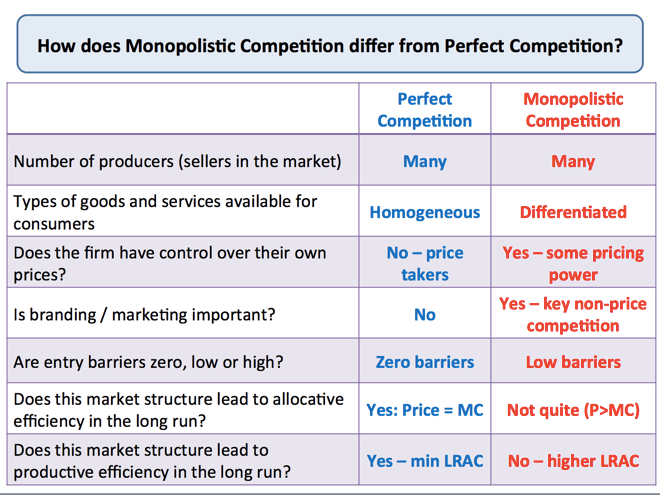

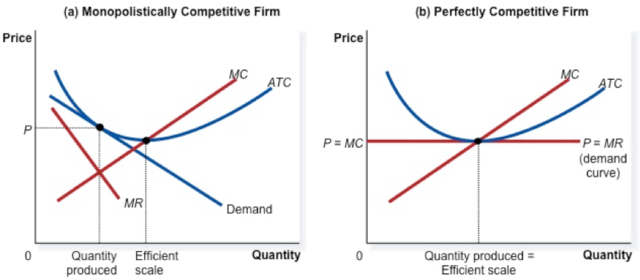

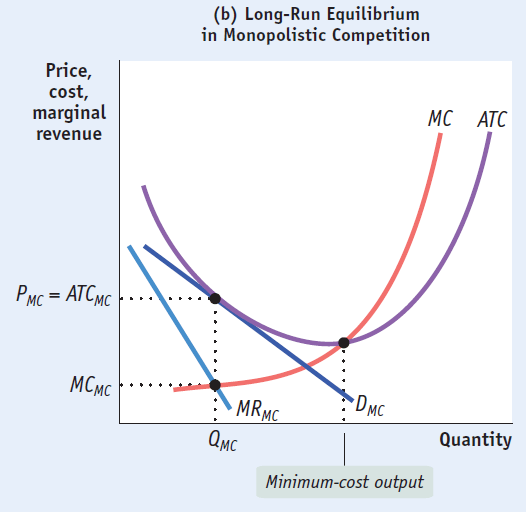

- Monopolistic competition operates to the left of minimum-cost output and has excess capacity